Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

Hong Kong SAR

Hong Kong SAR

Australia

Australia

Austria

Austria

Belgium

Belgium

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Hong Kong SAR

Greece

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Kingdom

United Kingdom

United States

United States

巴西

巴西

葡萄牙

葡萄牙

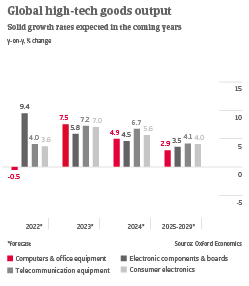

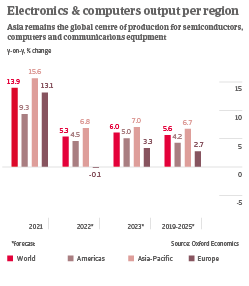

High-tech expansion. ICT electronics is an innovative and technology-driven industry. In particular, the semiconductor segment is highly value-added -- and provides robust margins for manufacturers. Expanding semiconductor production is a strategic target in both the US and the EU. US Congress recently passed a “Chips Act” worth USD 52 billion in order to prop up domestic leading edge semiconductor production. In February 2020, the EU Commission announced it will invest a total of EUR 45 billion in chip-related R&D, infrastructure and production until 2030.