Ongoing issues, but a strong automotive rebound expected in 2022

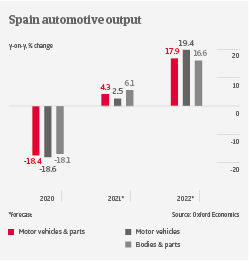

After contracting 18.6% in 2020, motor vehicles output is forecast to rebound by only 2.5% in 2021, as the current semiconductor shortage severely affects production. While car sales rebounded year-on-year between January-August 2021, they were 33% lower than in the same period of 2019, due to ongoing consumers’ uncertainty and less supply. Profit margins of businesses have increased in H1 of 2021 thanks to improved cost structures, but have started to decrease since then, due to semiconductor shortage, logistic bottlenecks and higher prices for raw materials and energy.

While production shortfalls have recently worsened, a strong rebound is expected in 2022, with output increasing 18%. The industry should benefit from the upcoming disbursement of the Next Generation EU fund, supporting suppliers in their shift towards e-mobility. Additionally, the Spanish government has announced public and private e-mobility investments worth EUR 24 billion over the coming three years.

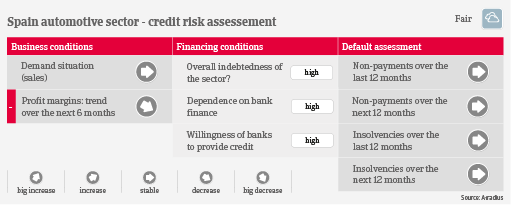

Spanish automotive businesses remain highly dependent on bank funding or other external financing sources, in order to finance high level of stocks and large investments in fixed assets. While the gearing of many companies has increased in 2020, banks have supported businesses. Backed-up by government guarantees, they provided long-term loans with grace periods of 1-2 years.

Payments in the automotive industry take 60 - 90 days on average. Payment behaviour has been good over the past two years, and both payment delays and insolvencies are not expected to increase in the coming months. However, should the current chip shortages and production cuts continue in 2022, smaller Tier 2 & 3 suppliers with limited access to new financing could face higher default risk.

Our underwriting stance is open for OEMs and Tier 1 suppliers, while more cautious for Tier 2 & 3 suppliers. In this segment, the gearing of businesses and their capacity to deal with it are of major importance for underwriting decisions.