Atradius Atrium

直接存取您的保單資訊、信用限額申請工具及深入瞭解。

香港SAR

香港SAR

土耳其

土耳其

中国

中国

丹麦

丹麦

日本

日本

比利时

比利时

加拿大

加拿大

匈牙利

匈牙利

印度

印度

希腊

希腊

波兰

波兰

法国

法国

芬兰

芬兰

保加利亚

保加利亚

美国

美国

美国英国

香港SAR

美国英国

香港SAR

挪威

挪威

捷克共和国

捷克共和国

荷兰

荷兰

斯洛伐克

斯洛伐克

意大利

意大利

新加坡

新加坡

新西兰

新西兰

瑞士

瑞士

瑞典

瑞典

德国

德国

墨西哥

墨西哥

澳大利亚

澳大利亚

奥地利

奥地利

爱尔兰

爱尔兰

罗马尼亚

罗马尼亚

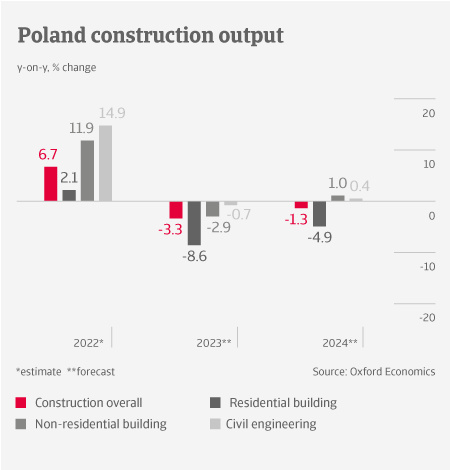

After growing 6.7% last year, Polish construction output is forecast to contract by more than 3% in 2023. Due to double-digit inflation rates the central bank has sharply increased interest rates, to 6.75% since September 2022. This had a negative impact on financing existing and new building projects. It also led to a major decline in mortgage loans, hitting residential construction in particular.

Many infrastructure projects are dependent on EU funding. However, the ongoing freeze of EUR 36 billion from the Next Generation EU fund (due to a dispute between the EU and Poland about rule-of-law issues) severely affects civil engineering activity. Commercial construction is affected by higher loan costs and the economic slowdown. That said, last year we saw a robust increase in industrial and warehouse construction.

Alongside lower demand, the construction sector suffers from high energy costs. After a sharp increase in 2021, prices for building materials have started to decrease in H2 of 2022, but remain elevated. Passing on higher input prices to customers is very difficult in a market characterised by fierce competition and a marked activity slowdown. Profit margins of construction businesses increased in 2020 and H1 of 2021, but have decreased since then, and we expect this downturn to continue in 2023.

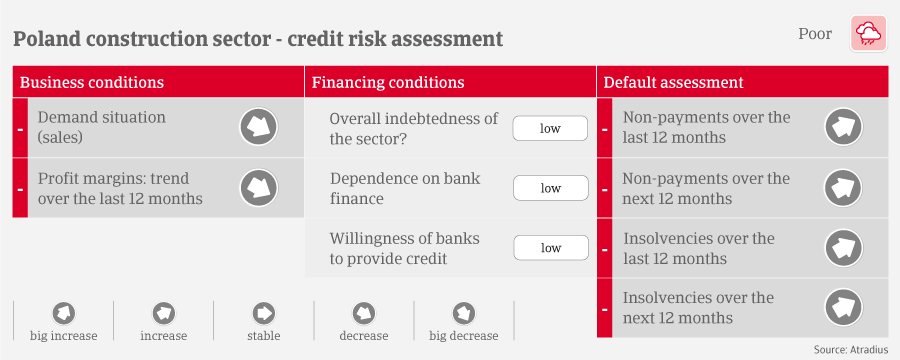

Payments in the Polish construction industry take 83 days on average. The sector is prone to payment delays, as there are many disputes related to quality and scope of work. Overdue payments of up to 30 days are common. Payment delays suffered by a company are usually passed on to peers along the value chain. Since H2 of 2022, we have observed a significant increase in non-payment notifications, and we expect this adverse trend to continue in 2023. Insolvencies are following the same trend, and we expect construction business failures to increase by more than 30% in 2023, due to the strained liquidity situation of many companies, coupled with decreasing demand. Most vulnerable are companies that have a low level of diversification in their work portfolio, and that are focused on infrastructure and/or residential construction.

Given the deteriorated credit risk situation and subdued business performance outlook for this year, our sector assessment remains “Poor” for the time being.