Atradius Atrium

直接存取您的保單資訊、信用限額申請工具及深入瞭解。

香港

香港

土耳其

土耳其

中國

中國

丹麥

丹麥

巴西

巴西

日本

日本

比利時

比利時

加拿大

加拿大

立陶宛

立陶宛

匈牙利

匈牙利

印度

印度

西班牙

西班牙

希臘

希臘

波蘭

波蘭

法國

法國

芬蘭

芬蘭

阿聯酋

阿聯酋

保加利亞

保加利亞

美國

美國

英國

香港

英國

香港

挪威

挪威

捷克共和國

捷克共和國

荷蘭

荷蘭

斯洛文尼亞

斯洛文尼亞

斯洛伐克

斯洛伐克

奧地利

奧地利

意大利

意大利

愛爾蘭

愛爾蘭

新加坡

新加坡

新西蘭

新西蘭

瑞士

瑞士

瑞典

瑞典

葡萄牙

葡萄牙

德國

德國

墨西哥

墨西哥

澳洲

澳洲

羅馬尼亞

羅馬尼亞

China’s trade credit landscape reflects a cautious response to a softer economic outlook and rising corporate liquidity strain. Survey data show that credit-based sales to business-to-business (B2B) customers account for under two in five transactions. This places China as the lowest user of B2B trade credit in Asia, broadly in line with Hong Kong and slightly below the average for Taiwan, while the other markets surveyed across the region report significantly higher shares. This pattern points to a more risk‑averse stance among Chinese suppliers.

Although trade credit usage has edged up in recent months, the increase has been more contained than across Asia, underlining a continued focus on limiting exposure to customer payment risk amid a challenging operating environment.

This caution is reflected in payment policies. China shows a stronger preference for shorter payment terms than the regional average, confirming a more cautious and risk‑averse approach to lenient payment policies than that of regional peers. A higher share of payments falls due within one month, while terms of up to two months are less common than across the region. Longer terms remain broadly aligned with Asia but are granted more selectively, often reserved for well-established trade relationships.

Overall, Chinese suppliers support B2B trade through credit, but stand out for strict payment risk control, mirroring patterns seen in Japan. This leads to a clear priority, protecting cash flow rather than supporting sales through more lenient terms. The macroeconomic backdrop reinforces this stance. Slowing domestic demand, weaker external conditions and heightened geopolitical uncertainty continue to weigh on corporate confidence. This environment encourages firms to safeguard liquidity, tightening credit conditions despite competitive pressures.

Despite maintaining tighter payment terms and a more cautious approach to trade credit, far more companies in China than across the region report a deterioration in the payment behaviour of B2B customers in recent months. Fewer report no change, pointing to a more unsettled payment environment, while the remainder reports improvement, broadly in line with the regional pattern. This creates a more uneven landscape, where payment behaviour improves for some customers but worsens for others, reinforcing the fragmented picture already evident in the market.

Reflecting this, more than four in five Chinese suppliers, particularly in the construction sector, report delayed payments from business customers, with around one third of invoices overdue, above the regional average. Among the markets surveyed, China ranks among the most affected by delayed payments, with only Taiwan and India reporting higher levels. Trend data points to an upward trend in overdue B2B receivables in recent months, suggesting that payment delays are becoming more widespread in China, and highlighting a clear gap between payment terms offered by suppliers and actual payment behaviour.

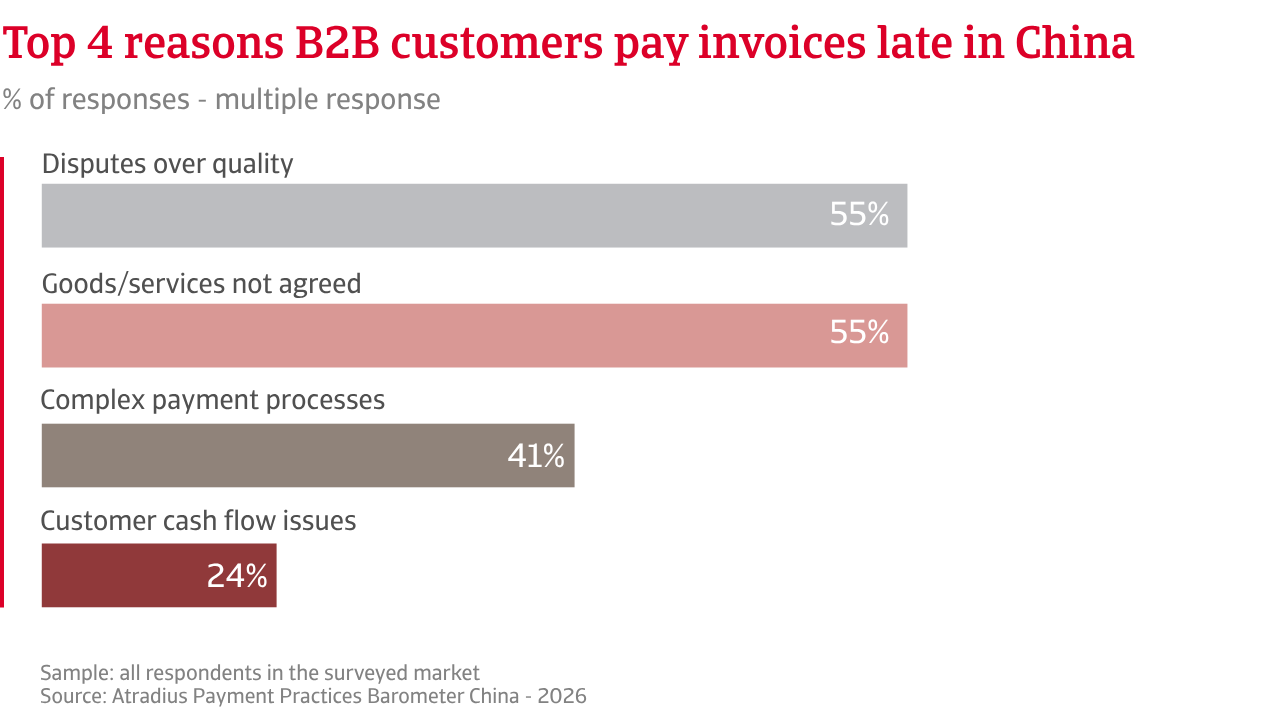

Days Sales Outstanding (DSO) data confirms this pattern. While most B2B invoices in China are still collected within one month, a meaningful share takes longer to settle, with more payments extending beyond two months than agreed payment terms would suggest. This indicates that once delays occur, they tend to significantly lengthen payment collection cycles. Unlike in other markets, payment delays in China are driven less by liquidity constraints and more by disputes over quality and delivery, which slow settlement. As a result, collection performance is uneven, with faster payments for some B2B customers alongside longer delays for others.

Strict credit management does not fully mitigate the risk of bad debt. A higher share of companies in China than across Asia reports credit losses above 5% of receivables, reflecting cases where long-overdue delayed payments turn into losses. Write‑offs are most often linked to legal disputes, confirming that payment delays typically stem from disagreements over quality and delivery rather than financial distress. The relatively limited role of receivable ageing as a reason for write-offs suggests that losses tend to occur before invoices become very old. This aligns with the wider pattern, where payments are either resolved or quickly escalate into defaults.

A higher share of companies in China than across Asia reports credit losses above 5% of receivables, reflecting cases where long-overdue delayed payments turn into losses.

The consequences for working capital are significant. Chinese businesses face similar pressure on cash flow as elsewhere in Asia, but they are less likely to rely on external financing or delay payments to suppliers. Instead, the main impact of customer payment risk on working capital is a strong constraint on investment and growth, suggesting that businesses tend to absorb financial strain internally rather than passing it through the supply chain. Tightly controlled liquidity management limits the impact of risk, but also highlights a clear trade‑off, with financial stability achieved at the expense of business growth.

Risk mitigation strategies reflect this balance. Chinese businesses focus on payment risk prevention, tightening terms, offering early payment incentives, and making greater of credit insurance than their regional peers do. This combination allows firms to protect against unpredictable outcomes in a payment environment shaped by disputes and long-overdue payments.

China’s trade credit system is therefore defined by credit control and selective approach to trading on credit with B2B customers. Chinese suppliers maintain tight control over payment risk exposure, although ongoing payment delays and heightened non-payment risk appear to weigh heavily on profits and investment.

Most businesses in China do not expect any meaningful change in B2B payment behaviour in the coming months. Among those anticipating a shift, more companies expect a slight improvement than deterioration, broadly in line with expectations across Asia. However, sentiment in China remains more guarded, reflecting uncertainty about the pace of any recovery. This caution stems from the recently observed payment patterns, where ongoing payment delays and bad debt write-offs continue to weigh on business confidence, suggesting that any improvement is likely to be gradual. The outlook therefore points to slower and less certain progress in China than across the wider region.

This uncertainty is reinforced by insolvency expectations. Across Asia, views are more evenly balanced between stability and further increases, while In China, more companies expect insolvencies to rise in the months ahead, pointing to a significantly weaker underlying payment environment. This helps explain why Chinese firms anticipate a more uneven recovery in B2B payment behaviour as the year unfolds, with improvements likely to occur alongside continued stress among more vulnerable B2B customers.

Profitability expectations mirror this opinion. Fewer firms in China expect profits to remain unchanged, indicating greater volatility in demand and payment conditions. While some businesses, particularly larger industrial firms, benefit from tighter credit control and relatively fast collections that support profit growth, a significant group of smaller companies faces elevated payment risk. This raises the likelihood of margin erosion and explains why more firms in China expect profitability to decline than across Asia.

When asked to indicate the risks they expect to severely disrupt B2B payment behavior in the months ahead, companies across Asia tend to focus on macroeconomic threats such as economic slowdown and inflation. In contrast, Chinese firms place greater emphasis on operational and non‑financial risks, most notably cybersecurity and fraud, which are cited far more frequently than in the region. Geopolitical instability also features more prominently in China, while supply chain disruptions and sector‑specific downturns are seen as less critical.

This points to a significantly different payment risk environment. Disruption in China is driven less by broad economic conditions and more by practical, day‑to‑day problems in how business transactions are carried out. This leads Chinese firms to tighten credit control and focus on preventing risk, as challenges come more from operations than from the wider economy.

For a full overview of the 2026 survey results for China, please download the market specific report from the related documents section below. Insights into Asia are available in the related content section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.