Atradius Atrium

直接存取您的保單資訊、信用限額申請工具及深入瞭解。

香港

香港

土耳其

土耳其

中國

中國

丹麥

丹麥

巴西

巴西

日本

日本

比利時

比利時

加拿大

加拿大

立陶宛

立陶宛

匈牙利

匈牙利

印度

印度

西班牙

西班牙

希臘

希臘

波蘭

波蘭

法國

法國

芬蘭

芬蘭

阿聯酋

阿聯酋

保加利亞

保加利亞

美國

美國

英國

香港

英國

香港

挪威

挪威

捷克共和國

捷克共和國

荷蘭

荷蘭

斯洛文尼亞

斯洛文尼亞

斯洛伐克

斯洛伐克

奧地利

奧地利

意大利

意大利

愛爾蘭

愛爾蘭

新加坡

新加坡

新西蘭

新西蘭

瑞士

瑞士

瑞典

瑞典

葡萄牙

葡萄牙

德國

德國

墨西哥

墨西哥

澳洲

澳洲

羅馬尼亞

羅馬尼亞

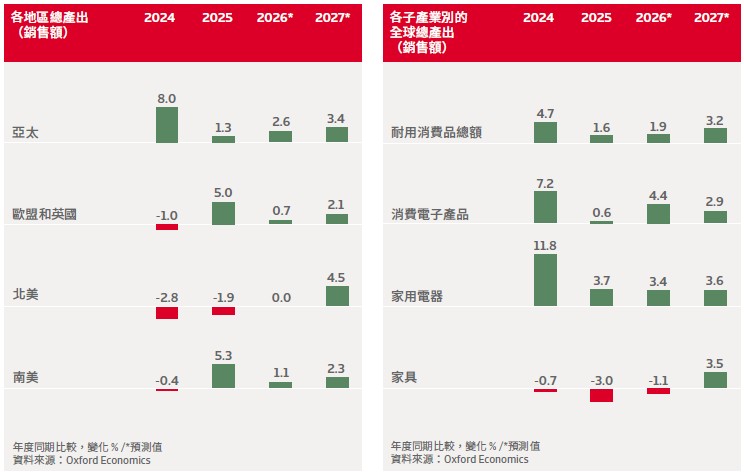

荷姆茲海峽的封鎖已推升全球大部分地區的油價。加上天然氣、肥料與農產品價格的上漲,全球消費者物價指數 (CPI) 通膨率將在 2026 年第二季攀升至 4.4% 的高峰,這對於一般家庭而言無疑是雪上加霜。

能源與糧食價格上漲壓縮了可支配所得,並將導致非必要支出減少;許多家庭不僅比以往更傾向儲蓄,並且延後或取消了大筆開支。因此,家電與家具產品的銷售將受到負面影響,消費電子產品也同樣難以倖免。

同時,耐用消費品製造商也面臨能源及特定原物料成本上升的壓力。

一旦波灣衝突一時間難以平息 – 假設油價在四個月內持續高於每桶 150 美元,並伴隨精煉能源產品供應短缺 – 2026 年全球通膨率將上升至 7.7%。在此情況下,全球耐用消費品銷售成長率將降至 0.4%,比目前預期低 1.5 個百分點。

許多先進市場耐用消費品零售業者的信用風險仍然很高,其中規模較小的零售業者特別容易發生違約和無力償債等問題。整個產業別所處經營環境競爭激烈,利潤不高。

美國私人消費成長率預計將從 2025 年的 2.6% 放緩至今年的 1.7%。能源成本上漲對核心物價的傳導效應將在未來幾個月內逐漸顯現,預計 2026 年美國消費者物價將上漲 3.3%。汽油價格上漲與物價通膨雙重因素將侵蝕實質收入,進而壓抑家庭支出。

短 期內,美國消費品的生產預計將維持低迷,且預測 2026 年耐用消費品的銷售額將萎縮 0.4%。非必需品支出以及對耐用財的需求最易受當前局勢影響;當能源價格、通膨與市場不確定性升高時,消費者通常會延後高單價商品的購買。

然而,目前家用電器、電子產品及家具的銷售價格已明顯高於長期趨勢水準。多數進口商既無法要求供應商降價,也無法自行吸收關稅所提高的成本,進而侵蝕其利潤空間。因此,儘管零售商犧牲部分利潤以吸收部分額外成本,但最終大多數仍轉嫁給了消費者。然而,目前家用電器、電子產品及家具的銷售價格已明顯高於長期趨勢水準。多數進口商既無法要求供應商降價,也無法自行吸收關稅所提高的成本,進而侵蝕其利潤空間。因此,儘管零售商犧牲部分利潤以吸收部分額外成本,但最終大多數仍轉嫁給了消費者。

儘管少數美國生產商確實掌握了更強的定價權,但同時關稅也增加了國內製造商的投入成本(例如金屬)。整體而言,美國將耐用消費品生產線遷回國內的選擇相當有限,主因是美國製造商缺乏基礎設施與專業技能,難以在短期內擴大生產規模,同時勞動成本也是一大挑戰。

展望 2027 年,隨著經濟與家庭消費成長力道轉強,預計耐用消費品市場將出現 5% 的強勁反彈,零售銷售額亦將成長2.5%。

中國零售市場目前是全球第二大消費市場,2025 年消費品零售總額達到 50.12 兆人民幣(約 6.23 兆歐元)。實體商品的網路零售額持續超越線下成長,其中即時零售(30 分鐘至 1 小時送達)正成為主要動能。此外,各大線上平台也正在擴大低毛利、高頻率的銷售模式。

然而,該方案帶來的動能已逐漸消退,儘管 2026 年初因農曆新年需求而有所提振,但我們預計 2026 年耐用消費品銷售額只會成長 2.5%。到了2027 年,我們預期耐用消費品產業將成長 3.2%

相較於許多其他區域的國家,儘管中國相對較能抵禦波灣戰爭所引發的全球能源衝擊,但第二輪外溢效應的跡象已開始顯現。除此之外,整體而言中國消費者信心依然波動,主要原因在於房地產業持續存在的問題:由於價格壓力,購屋者正面臨負財富效應。

通貨緊縮的環境、薪資成長疲弱以及較高的失業率,也進一步抑制了消費支出的成長,尤其對高單價商品的消費影響更為明顯。

繼 2025 年下滑 6.4% 後,中國家具製造業預計在 2026 年將進一步萎縮 3.7%。房地產市場問題與美國關稅則持續對家居用品出口造成壓力。

在經歷 2024 年與 2025 年的大幅下滑後,我們預計日本耐用消費品銷售額在2026 年僅會年增 1.9%,並於 2027 年趨於平穩。儘管政府已採取諸如汽油補貼等措施,以緩解能源價格上漲對消費者的衝擊,但能源成本居高不下仍將限制民間消費,特別是對於耐用消費品的衝擊更為明顯。

長遠來看,人口老化和人口規模下降代表著消費前景疲軟。

在經歷兩年疲弱表現後,我們預期 2026年法國耐用消費品銷售將再次萎縮 1.8%。國內消費正受到波灣戰爭及持續的政治不確定性影響。

零售業的信貸風險依然偏高。由於需求低迷,庫存水準相當高,而金融合作夥伴對短期融資的限制也日益嚴格。各個子產業的利潤率整體偏低,但小型家用電器領域的利潤率則高於消費電子產品。

小型零售商的付款延遲與破產情況依然嚴峻。相較之下,大型專業零售集團的財務狀況較為穩健,且市佔率持續擴大。

我們預期 2026 年德國零售銷售成長將放緩至 0.1%,耐用消費品銷售則將萎縮 2.1%。受波灣衝突影響,消費者信心已出現惡化;燃料價格急劇上漲並預計將傳導至其他產業,進一步侵蝕消費者的購買力。

通膨壓力的回升、高度的不確定性以及勞動市場的疲軟,將對消費決策造成壓力,特別是對非必需消費品的影響更為明顯。家庭財務若再度承受壓力,將有可能進一步抑制消費。

對於過去幾年原本就因較高的信貸風險而陷入困境的產業來說,所有這些因素都將對其造成衝擊。尤其是零售業正面臨投入成本偏高、信貸成本昂貴以及利潤率微薄等困境。

2025 年及 2026 年初的付款延遲與破產案例已處於高檔,且由於市場前景不利,我們預計未來幾個月相關數據將進一步升高。

我們預期英國私人消費成長今年將放緩至0.4%,而耐用消費品銷售將萎縮1.1%。

我們預期今年家庭實質收入將下降 0.2%,這將是自 2022 年以來最為疲弱的表現。由於不確定性持續存在,消費者正採取更為審慎的觀望態度,並延 後大筆的開支。

該領域的信用風險依然偏高,因此透過庫存與供應鏈管理來保持強健的流動性紀律,將是致勝關鍵。在萎縮的市場中,規模較小的業者受創最嚴重,這是因為許多業者無法爭取到較有利的價格和付款條件。

全球: 能源與糧食價格上漲壓縮了可支配所得,並將導致非必要支出減少;許多家庭不僅比以往更傾向儲蓄,並且延後或取消了大筆開支

美國: 短期內,美國消費品的生產預計將維持低迷,且預測 2026 年耐用消費品的銷售額將萎縮 0.4%

中國: 通貨緊縮的環境、薪資成長疲弱以及較高的失業率,也進一步抑制了消費支出的成長,尤其對高單價商品的消費影響更為明顯

法國: 在經歷兩年疲弱表現後,我們預期 2026 年法國耐用消費品銷售將再次萎縮 1.8%

德國: 通膨壓力的回升、高度的不確定性以及勞動市場的疲軟,將對消費決策造成壓力,特別是對非必需消費品的影響更為明顯

英國: 在萎縮的市場中,規模較小的業者受創最嚴重,這是因為許多業者無法爭取到較有利的價格和付款條件