The forint remains vulnerable to international investors’ sentiment due to the elevated external and public debt levels and institutional issues.

Political situation

Troublesome relationship with the EU remains

The ruling conservative coalition of the Fidesz and KDNP parties under Prime Minister Viktor Orbán has repeatedly taken actions that led to confrontations with the EU commission and its EU peers (e.g. a controversial media law, some constitutional amendments curbing judicial independence, a tough stance in the migrant policy and a pro-Russia stance. Together with some unorthodox economic policy decisions like additional taxes on banks, the government’s repeated confrontations with the EU have led to some uncertainty among its European peers and international investors in the past.

In the April 2018 general elections the coalition government won again, and with its two-thirds majority in parliament it can alter the country’s constitution all by itself.

Economic situation

Decelerating growth in 2020

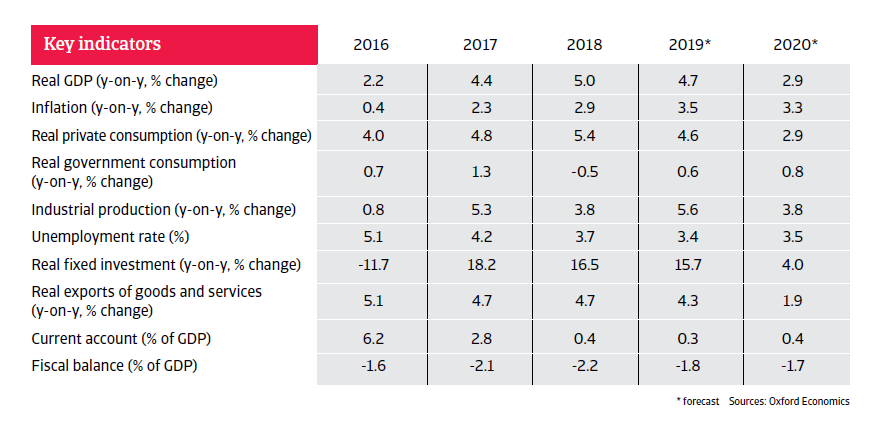

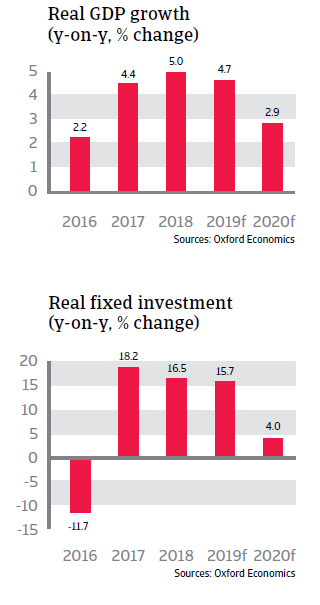

In 2019 economic growth is expected to remain robust, driven by high levels of investment, while private consumption and export remain solid. However, in 2020 GDP growth is expected to decelerate below 3% due to lower household consumption, a marked slowdown in investment activity, and lower export growth, as demand from Hungary’s main export markets is decreasing. Consumer prices started to rise again in 2017 and 2018, and are forecast to remain above 3% in 2019 and 2020, mainly because of robust wage growth over the last two years.

Containing the budget deficit to 3% of GDP is a top priority of the administration in order to avoid EU sanctions. However, since 2010 the government has been using unorthodox ways to balance the budget, most notably extraordinary taxes on banks and utilities. The budget deficit is forecast to decline modestly in 2019 and 2020. Despite annual decreases, public debt remains high at about 68% of GDP in 2019. (Central-Eastern Europe median is about 50% of GDP).

High external debt level remains a major weakness

Hungary’s major weakness remains its elevated level of external debt (about 80% of GDP in 2019). A large share of this debt is foreign currency-denominated, which exacerbates the problem, as a sharp forint depreciation would hurt many Hungarian households and businesses whose loans are denominated in foreign currencies. Additionally, more than 30% of public debt is denominated in foreign currency. The forint remains vulnerable to international investors’ sentiment due to the elevated external and public debt levels and a suboptimal institutional and policy environment.

相關資料

4.67MB PDF