Supply chain pressures, but higher vehicle sales prices sustain margins

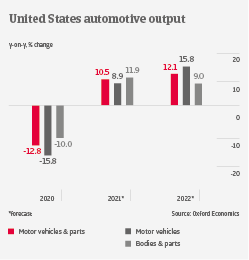

After declining 27.9% in 2020, US car sales are expected to grow only 7.5% this year, as supply issues thwart robust demand. Low production growth in 2021 is mainly due to semiconductor shortage, and the impact of Hurricane Ida on petrochemical companies has caused supply constraints of plastics. While semiconductor shortage is expected to last into 2022, output of vehicles is forecast to grow 12% next year.

In order to maintain profits, Original Equipment Manufacturers (OEMs) have adjusted their production by prioritising high-margin and most demanded models (e.g. trucks). They have also been able to increase sales prices for vehicles. Margins of suppliers have come under pressure due to production shortfalls, higher prices for materials and labour shortage, while at the same time fixed costs remain high. However, a major deterioration of margins is not expected, as suppliers also benefit from ongoing demand and higher sales prices.

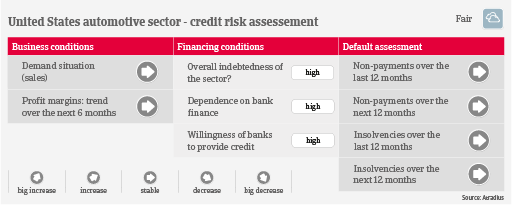

Being a capital-intensive industry, automotive is dependent on bank finance, and many businesses are highly leveraged. Currently banks are very willing to provide loans to the sector. Increased competition among financial institutions has led to loosened lending standards over the last couple of months. Payments in the automotive industry take about 60 days on average. During the pandemic-related shutdowns in 2020, businesses have stretched payments in order to preserve cash, but meanwhile the majority of companies has returned to normal payment terms. The level of payment delays and insolvencies has been low over the past couple of months, and no substantial increase is expected in 2022.

Taking into account the current challenges for the sector, but also its financial resilience, our sector assessment remains “Fair”. The Biden administration plans to support e-mobility by investing USD 174 billion in charging stations, mass transit vehicles and school buses. Large OEMs have announced to launch more electric vehicles and large investments in battery plants.