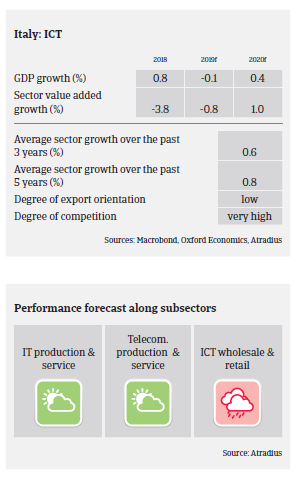

The Italian ICT wholesalers and retail segment is negatively impacted by stiff competition, high pressure on margins and liquidity management issues.

- According to the industry association Assinform, IT services sales grew 0.7% year-on-year in 2018, to EUR 30 billion, and in 2019 a 1.6% increase is expected. The e-commerce market grew 24%, to EUR 28 billion, with 16% growth expected in 2019.

- The economic slowdown and lower business investments will have an impact in 2019, as tighter cost controls could lead to lower ICT expenditures made by small- and medium-sized businesses and public bodies. However, ICT investments by large companies are expected to remain stable, and those alone account for 50% of total domestic ICT investments.

- In most ICT segments margins remained stable in 2018, and are expected not to decrease in 2019. Due to rather modest organic growth opportunities and market adjustment in the distribution segment, companies strive to expand through acquisitions and specialisation (customised and value-added services).

- Both financial gearing and dependence on bank loans are high in the Italian ICT sector. While payments in the industry generally take around 110 days, payment experience has been good over the past two years, and the level of notified non-payments is still low. The amount of ICT business failures is rather low compared to other Italian industries, and while Italian business insolvencies are forecast to increase 6% year-on-year in 2019, ICT business failures are expected to level off.

- Our underwriting approach remains generally open for most IT and telecommunication producers and service providers due to the benign credit risk situation, the general need of Italian businesses to increase IT spending in order to boost productivity and increasing demand for innovation (digitalisation, cybersecurity, Big Data, electronic payments, cloud computing).

- However, smaller players have to be monitored more closely, as they are more exposed to financial distress related to working capital requirements, especially when depending on large clients and the public sector.

- For several months we have adopted a more restrictive approach to the ICT wholesalers retail segment, especially on companies with low value added services and a weak position in the value chain. This segment is characterised by stiff competition, significant pressure on margins and liquidity management issues. Non-payment notifications in this subsector have increased in early 2019.

相關資料

Market Monitor ICT 2019

1.13MB PDF