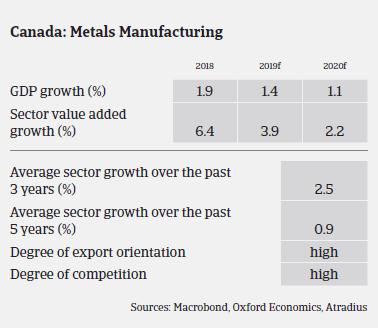

The sector benefits from the lift of US import tariffs on Canadian steel and aluminium, with profit margins of steel businesses expected to improve again.

In H1 of 2019 most Canadian metal and steel businesses showed positive results, with higher revenues due to higher sales prices, robust demand and the impact of protectionist measures in both Canada and the US, which disadvantage competition from overseas suppliers.

The sector benefits significantly from Washington´s decision in May 2019 to lift US import tariffs on Canadian steel and aluminium (the US market accounted for 82% of all Canadian iron and steel exports in 2018, affecting about 45% of domestic production). In June 2019 alone Canadian exports of previously tariffed steel products to the US increased 15.8% year-on-year, while exports of aluminum products rose 47.2%. Profit margins of Canadian metal and steel businesses are expected to improve over the coming 12 months.

As in 2018, payments in the Canadian metals and steel sector take 65 days on average, and payment experience has been good over the past two years. However, it cannot be ruled out that due to weaker economic growth prospects and lower demand from key buyer sectors (construction and energy) payment delays could increase in 2020. However, so far this adverse development has not yet materialised. No major insolvency increase is expected over the coming 12 months.

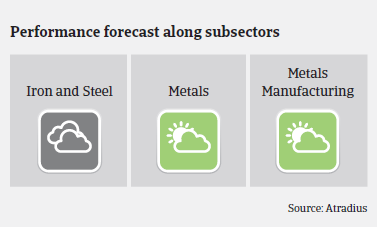

Our underwriting stance remains neutral for the steel segment. Many companies are foreign-owned, and for the few remaining Canadian-owned companies we seek detailed financial disclosure due to concerns about the cyclical and capital-intensive nature of the business (several companies have sought insolvency protection in the past). While the lifting of the US protectionist tariffs is positive, concerns over overcapacity remain.

For the metals segment our underwriting stance remains open, as this subsector provides more value-added products and overcapacity is less of an issue compared to the steel segment.

相關資料

1.06MB PDF